Europe Textile Market Report Summary

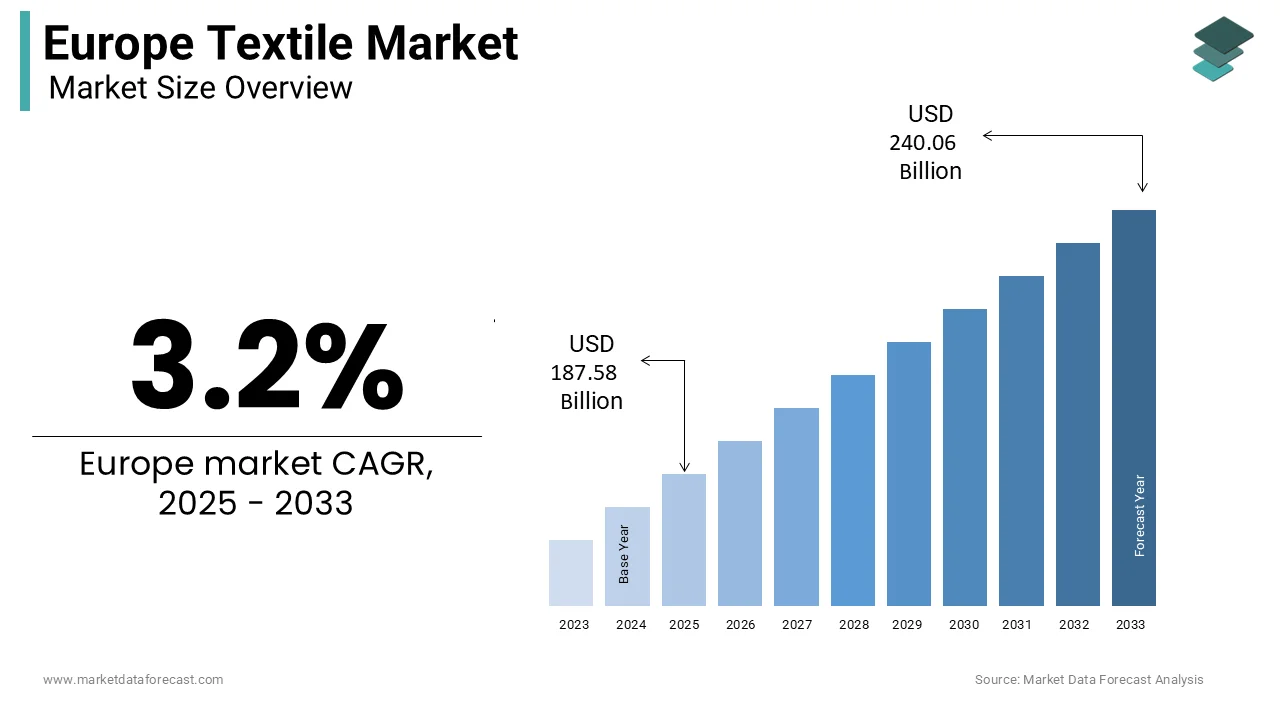

The European textile market was valued at USD 181.77 billion in 2024, is estimated to reach USD 187.58 billion in 2025, and is projected to reach USD 240.06 billion by 2033, growing at a CAGR of 3.2% from 2025 to 2033. The growth of the European textile market is driven by the rising demand for sustainable and high-performance fabrics, expanding apparel and fashion industries, and technological advancements in textile manufacturing. Increasing consumer awareness of eco-friendly materials, coupled with government initiatives promoting circular economy practices and recycling in textiles, is reshaping the European textile landscape.

Key Market Trends

- Rising adoption of sustainable fibers such as organic cotton, bamboo, and recycled polyester to meet EU sustainability targets.

- Increasing digitalization and automation in textile production, improving efficiency and design flexibility.

- Growing prominence of technical textiles for automotive, medical, and industrial applications.

- Surge in fast fashion brands transitioning to circular supply chains with recyclable and traceable materials.

- Expanding influence of e-commerce platforms and direct-to-consumer models in textile retail.

Segmental Insights

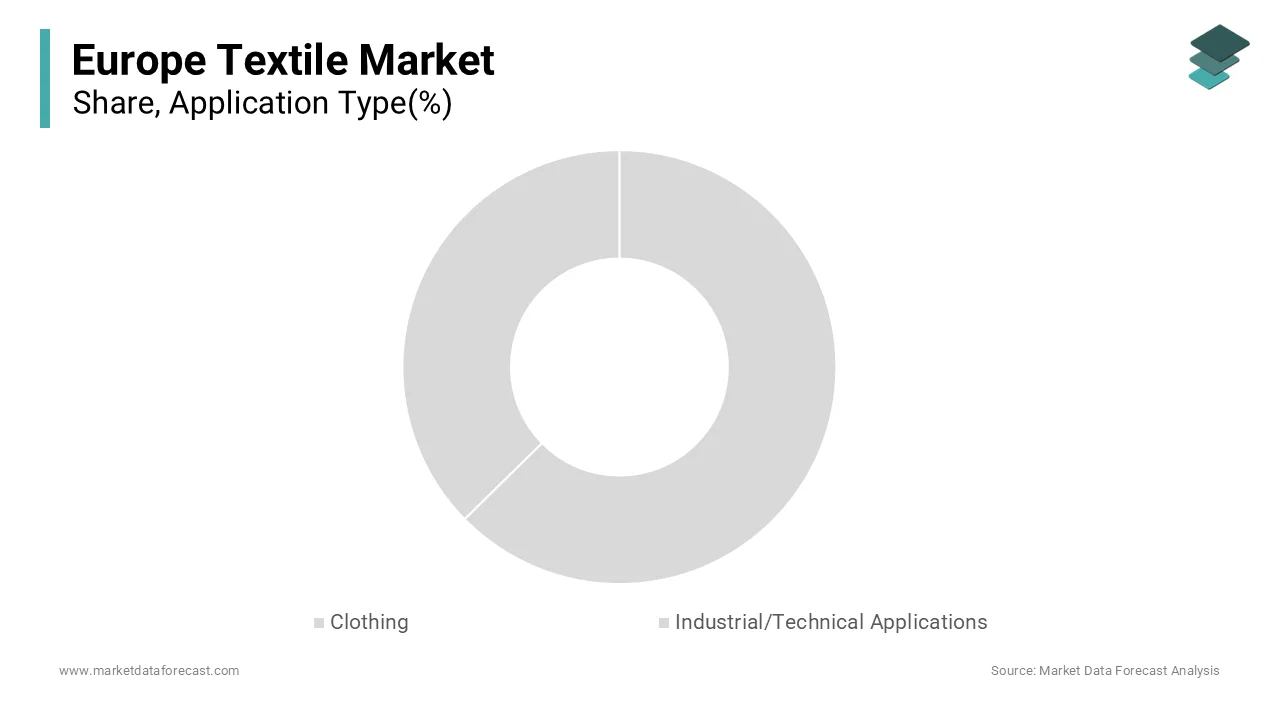

- Based on application type, the clothing segment dominated the European textile market by accounting for 48.1% share in 2024. The dominance of this segment is attributed to Europe’s strong fashion and luxury industries, high consumer spending on apparel, and the rising popularity of athleisure and functional wear.

- Based on material type, the synthetics segment led the European textile market by capturing a 52.5% share in 2024. Synthetic textiles such as polyester, nylon, and acrylic continue to hold a strong position due to their durability, affordability, and versatility across both apparel and industrial applications.

- Based on process type, the woven textiles segment was the prominent segment in the European textile market and captured a share of 64.7% in 2024. This segment’s strength lies in its use across a variety of sectors, including fashion, home furnishings, and automotive interiors, where precision, strength, and design versatility are essential.

Regional Insights

The European textile market is experiencing steady growth across major economies, supported by industrial modernization and the shift toward sustainable materials.

- Germany outperformed other regions in the European textile market and accounted for an 18.5% share in 2024, driven by its leadership in technical textiles, advanced manufacturing technologies, and export-oriented production.

- Italy continues to be a hub for premium and luxury fabrics, with strong craftsmanship traditions and globally recognized fashion houses.

- France maintains steady growth due to its strong fashion industry and government support for eco-friendly textile innovation.

- Spain and Portugal are emerging as important production centers for fast-fashion brands, supported by nearshoring trends and cost-efficient manufacturing.

- The Nordic countries are at the forefront of sustainable textile innovation, focusing on bio-based materials and circular production processes.

Competitive Landscape

The European textile market is highly diverse and innovation-driven, with established players focusing on sustainability, digital transformation, and advanced fiber technologies. Leading companies are investing in recycling infrastructure, smart fabrics, and biodegradable materials to align with EU sustainability directives. Collaboration between apparel brands, textile producers, and chemical companies is further driving value-chain integration and resource efficiency. Prominent players in the Europe textile market include Lenzing AG, H&M Group, Inditex (Zara), Kering SA, Adidas AG, Hugo Boss AG, Marzotto Group, Aquafil S.p.A., Prada S.p.A., Freudenberg Group, BASF SE, Toray Industries, Inc., Teijin Limited, Klopman International S.r.l., and Tessitura Monti S.p.A

Europe Textile Market Size

The europe textile market was valued at USD 181.77 billion in 2024, is estimated to reach USD 187.58 billion in 2025, and is projected to reach USD 240.06 billion by 2033, growing at a CAGR of 3.2% from 2025 to 2033.

A textile is any material made from interlacing fibers, including natural or synthetic yarns and threads, that can be processed into a fabric or other product. Deeply rooted in regional industrial traditions, the sector is now undergoing a structural metamorphosis shaped by sustainability imperatives, digital transformation, and evolving regulatory frameworks. According to sources, the European Union imported textile and clothing products valued at substantial billions of euros in 2022, which emphasizes its integration into global supply networks while retaining pockets of high-value domestic production in Italy, Germany, and Portugal. The 2022 Strategy for Sustainable and Circular Textiles mandates that all textile products placed on the EU market by 2030 must be durable, repairable, and recyclable. Concurrently, consumer behavior is shifting decisively.

MARKET DRIVERS

Rising Consumer Demand for Sustainable and Circular Textiles

European consumers are increasingly prioritizing environmental and ethical considerations in their purchasing behavior, which creates a powerful impetus for sustainable textile innovation and thereby drives the growth of the Europe textile market. According to the European Commission’s 2023 Eurobarometer survey on the circular economy, 77 percent of EU citizens believe that extending the life of clothing through reuse and repair significantly benefits the environment. This attitudinal shift is translating into concrete market action. Regulatory mechanisms are reinforcing this trend. France’s Anti-Waste Law for a Circular Economy, effective since 2022, prohibits the destruction of unsold non-food goods, compelling brands to redirect surplus inventory toward donation or recycling streams. Germany’s Green Button certification scheme, adopted by more than 150 companies as of 2023, exemplifies how policy and consumer expectations jointly drive supply chain transparency. These converging forces are accelerating investment in closed-loop systems, organic cotton cultivation, and bio-based synthetics, fundamentally reshaping product development and procurement strategies across the continent.

Digitalization and Industry 4.0 Integration in Textile Manufacturing

The adoption of advanced digital technologies is redefining efficiency, customization, and agility in European textile production, which propels the expansion of the Europe textile market. As per research, a majority of textile producers across Europe have already incorporated advanced Industry 4.0 technologies such as connected machinery, artificial intelligence tools, and digital simulation platforms. According to sources, manufacturers in Germany are increasingly using smart factory systems that improve energy efficiency and enhance production speed through predictive monitoring and data analytics. As per research, textile companies in Italy are widely adopting automated weaving and cloud-based systems, allowing them to stay flexible and respond quickly to shifting fashion demands. According to sources, digital design technologies are also reducing material wastage and cutting the need for physical prototypes across the European apparel sector. Apart from these, on-demand 3D knitting and digital printing technologies are gaining traction, drastically reducing overproduction. This digital evolution not only enhances competitiveness against low-cost global rivals but also supports the EU’s broader decarbonization agenda by optimizing material and energy use.

MARKET RESTRAINTS

Stringent Environmental Regulations and Escalating Compliance Costs

It operates under an increasingly dense web of environmental regulations that impose significant financial and operational burdens, particularly on small and medium-sized enterprises, which constrains the growth of the Europe textile market. As per the European Environment Agency, EU textile producers must comply with major regulatory frameworks, including REACH for chemical safety, the Industrial Emissions Directive, and evolving EU Ecolabel criteria. The forthcoming EU ban on exporting textile waste to non-OECD countries will compel producers to internalize end-of-life management costs. The accumulation of ecologically driven mandates, while important, is stifling investment in innovation and posing a serious threat to the survival of traditional manufacturing hubs in Eastern Europe.

Intense Competition from Low-Cost Asian Textile Producers

The relentless competitive pressure faced by regional manufacturers from Asian exporters, whose advantages stem from lower labor costs, economies of scale, and state-backed industrial strategies, in turn slows down the expansion of the Europe textile market. Even with anti-dumping duties on certain Chinese synthetic fibers, the landed cost of polyester fabric from India remains cheaper than comparable EU-made alternatives, as per sources. Fast fashion retailers, which represent a portion of EU apparel sales, source a share of their garments from Asia due to cost and speed efficiencies, which further marginalize local producers. The European Apparel and Textile Confederation states that while nearshoring has seen some recent growth, EU manufacturers will be unable to compete in volume-driven markets unless they receive significant automation subsidies and changes to trade policy.

MARKET OPPORTUNITIES

Growth in Technical and Performance Textiles Across Industrial Sectors

Technical textiles are emerging as a key prospect for the expansion of the Europe textile market. This is driven by demand from automotive, healthcare, construction, and renewable energy sectors. As per research, technical textiles have become a key pillar of the European textile industry, now representing a larger share of total production value than traditional clothing or household fabrics. According to sources, the medical textile segment continues to experience strong growth across Europe, driven by the increasing use of high-performance materials such as antimicrobial and surgical fabrics, with Germany playing a significant role in production. In the automotive industry, lightweight composite fabrics are essential for electric vehicle manufacturing. The EU’s Green Deal is also accelerating adoption in construction, where geotextiles and insulation made from recycled PET are now mandated in public infrastructure projects under the Energy Performance of Buildings Directive. This diversification into engineered applications insulates European producers from fashion volatility and aligns with industrial sovereignty goals.

Revival of Localized and Artisanal Textile Production Through Policy Support

A renaissance of localized textile manufacturing is creating fresh opportunities for the expansion of the Europe textile market. This is supported by public investment, regional development funds, and rising consumer appreciation for heritage craftsmanship. Significant funding has been allocated across Europe to support the modernization of small textile workshops in rural regions such as Italy, Portugal, and Romania, helping preserve traditional crafts like hand weaving and natural dyeing, according to sources. Employment within artisanal textile clusters in these regions has continued to grow, reflecting rising consumer interest in authentic, locally produced fabrics, as per research. National initiatives promoting domestic textile branding are further strengthening this movement, encouraging mid-sized fashion labels to source more locally, according to sources. These localized ecosystems reduce transportation emissions, strengthen rural economies, and offer a culturally resonant alternative to mass-produced fast fashion, which positions artisanal textiles as both an economic and identity-driven opportunity.

MARKET CHALLENGES

Energy Price Volatility and Decarbonization Pressures

Regional producers are navigating severe operational instability caused by volatile energy markets and the urgent imperative to decarbonize energy-intensive processes, which challenges the growth of the Europe textile market. According to the European Central Bank, industrial electricity prices in the EU averaged 210 euros per megawatt hour in 2022, more than double 2020 levels, directly impacting cost structures in dyeing, finishing, and spinning. In addition, the EU Emissions Trading System has driven carbon allowance prices above 80 euros per ton of CO2 in 2023, as reported by the European Environment Agency, increasing compliance costs for fossil-fueled operations. The Fit for 55 package mandates a 55 percent reduction in industrial emissions by 2030, which requires massive capital investment in electrification and renewable integration, outlays that many small and medium enterprises cannot afford. Lack of a coordinated energy policy and a decarbonized grid will push production toward cheaper, yet more polluting, energy supplies elsewhere.

Fragmented Recycling Infrastructure and Low Fiber-to-Fiber Recovery Rates

Region lacks a cohesive and scalable textile recycling infrastructure, which severely limits the feasibility of true circularity and impedes the expansion of the Europe textile market. According to the European Environment Agency, less than 1 percent of post-consumer textile waste in the EU is currently recycled into new apparel-grade fibers, with the vast majority downcycled into low-value applications like insulation or cleaning rags. Chemical recycling technologies remain nascent. Moreover, municipal collection systems are highly inconsistent. This infrastructural fragmentation undermines circular business models and exposes brands to future non-compliance risks under the EU’s upcoming mandatory separate collection of textile waste, set to take effect in 2025. Europe will not achieve its circular textile goals unless it makes harmonized investments in advanced sorting, solvent-based recycling, and design-for-recycling standards.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2024 to 2033 |

|

Base Year |

2024 |

|

Forecast Period |

2025 to 2033 |

|

Segments Covered |

By Application Type, Material Type, Process Type and Region. |

|

Various Analyses Covered |

Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

|

Countries Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, and the Rest of Europe |

|

Market Leaders Profiled |

Lenzing AG, H&M Group, Inditex (Zara), Kering SA, Adidas AG, Hugo Boss AG, Marzotto Group, Aquafil S.p.A., Prada S.p.A., Freudenberg Group, BASF SE, Toray Industries, Inc., Teijin Limited, Klopman International S.r.l., Tessitura Monti S.p.A. |

SEGMENTAL ANALYSIS

By Application Type Insights

The clothing segment dominated the Europe textile market by accounting for 48.1% share in 2024. The dominance of the clothing segment is driven by Europe’s deeply embedded fashion culture, high per capita apparel expenditure, and the presence of global luxury brands headquartered in France and Italy. Germany and the United Kingdom are exhibiting notable expenditure. Apart from these, fast fashion retail continues to drive volume despite sustainability concerns. The segment is further reinforced by e-commerce growth. The European textile economy relies on clothing as its foundation, a status maintained by high daily demand and seasonal sales, along with brand innovation, despite ongoing regulatory changes.

The industrial or technical applications segment is on the rise and is expected to be the fastest-growing segment in the global market by witnessing a CAGR of 6.8% from 2025 to 2033. The rapid expansion of the industrial or technical applications segment is primarily fueled by cross-sectoral integration of high-performance textiles in automotive, medical, and renewable energy industries. In the automotive sector, lightweight composite fabrics are critical for electric vehicle efficiency. Furthermore, the EU’s Green Deal mandates increased use of geotextiles in sustainable infrastructure. These structural industrial shifts, coupled with policy support for strategic autonomy in critical materials, position technical textiles as the most dynamic application frontier in Europe.

By Material Type Insights

The synthetics segment led the European textile market by capturing a 52.5% share in 2024. The growth of the synthetics segment is attributed to the cost efficiency, durability, and functional versatility of polyester, nylon, and acrylic fibers, which are extensively used in both mass-market apparel and industrial applications. According to sources, a portion of garments sold in the EU contain polyester, valued for its wrinkle resistance and moisture-wicking properties. Besides, synthetic fibers benefit from established recycling streams. Fast fashion retailers rely heavily on synthetics due to short production cycles and low material costs. Synthetics are maintaining their market dominance in textiles, with innovations in bio-based polyesters and chemical recycling offsetting environmental concerns regarding microplastic shedding.

The cotton segment is expected to exhibit a noteworthy CAGR of 5.4% during the forecast period, owing to rising consumer and regulatory preference for natural, biodegradable fibers amid tightening EU sustainability rules. The European Commission’s Strategy for Sustainable and Circular Textiles mandates increased use of certified organic and recycled natural fibers, directly benefiting cotton. As per sources, licensed Better Cotton accounted for a portion of all cotton used by EU brands in 2023, up from a share in 2020. National policy support is also pivotal. Furthermore, innovations in efficient cultivation and traceability blockchain systems are addressing historical concerns around cotton’s environmental footprint. This confluence of regulatory tailwinds, consumer trust, and supply chain transparency is propelling cotton’s accelerated growth despite higher costs compared to synthetics.

By Process Type Insights

The woven textiles segment was the prominent segment in the Europe textile market and captured a share of 64.7% in 2024. The prominence of the woven textiles segment is fuelled by the extensive use of woven fabrics in high-value applications such as luxury apparel, tailored garments, and technical composites. Italy and Germany, Europe’s leading textile producers, specialize in high-precision woven fabrics for fashion and automotive interiors. Woven fabrics also offer superior dimensional stability and tensile strength, making them indispensable in industrial contexts. Apart from these, heritage craftsmanship in regions continues to sustain demand for artisanal woven textiles, supported by EU cultural preservation funds. The durability and recyclability of mono-material woven constructions further align with circular economy objectives, reinforcing their structural dominance across both traditional and advanced textile domains.

The non-woven segment is predicted to witness the highest CAGR of 7.2% from 2025 to 2033. The rapid growth of the non-woven segment is propelled by surging demand in hygiene, medical, and filtration applications, particularly in the aftermath of global health crises. According to research, non-woven production in Europe reached significant metric tons in 2023, with medical and hygiene uses accounting for 61 percent of output. During the pandemic, EU demand for non-woven surgical masks and gowns surged, and although acute needs have subsided, permanent shifts in healthcare protocols sustain baseline demand. Beyond healthcare, non-wovens are integral to battery separators in electric vehicles. Environmental innovations are also accelerating adoption. These multifaceted drivers position non-wovens as the most dynamic process technology in the European textile landscape.

COUNTRY LEVEL ANALYSIS

Germany Textile Market Analysis

Germany outperformed other regions in the European textile market and accounted for 18.5% share in 2024. The prominence of Germany is primarily driven by high-performance technical textiles and industrial fabrics. Germany is Europe’s largest producer of automotive textiles, supplying a portion of the continent’s interior and insulation materials for vehicles, according to studies. The nation’s engineering prowess extends to machinery. Trützschler and Karl Mayer, headquartered in Germany, dominate global textile machinery exports, reinforcing domestic production capabilities. Government support through initiative has allocated funds to advance smart and sustainable textiles. Apart from these, Germany’s stringent waste management laws have spurred investment in fiber recycling. Germany’s strong R&D infrastructure and deep integration into the automotive and medical industries ensure that its textile sector remains a foundation of European industry.

Italy Textile Market Analysis

Italy was the second largest in the Europe textile market and occupied a 16.5% share in 2024. The growth of Italy is led by its global leadership in luxury and high-end fashion textiles. The country produces a portion of the world’s luxury fabrics, with Como and Biella serving as epicenters for silk and fine wool weaving. Italian textile exports reached a notable amount in 2023, with a portion destined for premium fashion houses in France, the United States, and Asia, according to sources. The sector thrives on artisanal craftsmanship combined with digital innovation. National initiatives certification has strengthened brand equity. Despite labor shortages, Italy’s fusion of heritage and technology ensures its continued dominance in value-driven textile segments.

France Textile Market Analysis

France is a lucrative region in the European textile market due to its dual strength in haute couture and technical innovation. Home to global fashion giants like LVMH and Kering, France drives demand for premium natural fibers, silk, and wool imports for luxury apparel, as per studies. Simultaneously, France is a leader in medical and aerospace textiles. The government has invested a notable amount since 2021 to reshore textile production and support organic fiber farming. Notably, France pioneered the Anti-Waste Law banning unsold garment destruction, which causes circular business models across the EU. France’s robust policy frameworks and influential brands steer the cultural and regulatory future of the European textile industry.

United Kingdom Textile Market Analysis

The United Kingdom grew steadily in the Europe textile market owing to a strong design ecosystem and growing emphasis on sustainability. London remains a global fashion capital, hosting designers who increasingly prioritize traceable supply chains. Post Brexit, the UK has accelerated domestic textile revival. Academic institutions like the Royal College of Art drive innovation in biotextiles, with startups developing mycelium and algae-based fabrics. However, reliance on imported raw materials remains a vulnerability. Despite challenges, the UK’s creative capital and regulatory ambition position it as a laboratory for next-generation textile models.

Spain Textile Market Analysis

Spain is likely to grow in the European textile market due to fast fashion integration and regional artisanal clusters. The country is the production base for Inditex, the world’s largest fashion retailer, which sources a portion of its garments from Spanish and Portuguese mills, according to research. This proximity enables rapid restocking and reduced lead times, a key competitive advantage. Beyond fast fashion, regions like Galicia and Valencia preserve traditional linen and esparto grass weaving, now revitalized through EU rural development grants. Spain has also emerged as a hub for digital printing. Spain serves as a European leader in sustainable innovation by combining its rich cultural history with efficient, agile manufacturing.

COMPETITIVE LANDSCAPE

Competition in the Europe textile market is characterized by a dual structure featuring high-end luxury producers and agile fast fashion integrators alongside specialized technical textile manufacturers. The landscape is highly fragmented with thousands of small and medium enterprises coexisting with a few multinational players. Intensifying regulatory pressure on sustainability and circularity is reshaping competitive dynamics, favoring companies with transparent supply chains and recycling capabilities. Innovation in materials, such as bio-based fibers and digital production technologies, has become a key differentiator. Cross-border consolidation is increasing as firms seek scale to absorb compliance costs. At the same time, artisanal producers are carving niches through heritage craftsmanship and local storytelling. The entry of non-traditional players from the chemicals and waste management sectors is further disrupting traditional boundaries. This complex ecosystem demands strategic agility and long-term investment in both technology and sustainability to maintain relevance and growth.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the europe textile market include

- Lenzing AG

- H&M Group

- Inditex (Zara)

- Kering SA

- Adidas AG

- Hugo Boss AG

- Marzotto Group

- Aquafil S.p.A.

- Prada S.p.A.

- Freudenberg Group

- BASF SE

- Toray Industries, Inc.

- Teijin Limited

- Klopman International S.r.l.

- Tessitura Monti S.p.A.

TOP LEADING PLAYERS IN THE MARKET

- Loro Piana is a premier Italian luxury textile manufacturer renowned for its ultra-fine cashmere and vicuña fabrics. The company supplies high-end materials to global fashion houses and maintains vertically integrated operations from raw fiber sourcing to finished fabric. In recent years, Loro Piana has intensified its commitment to traceability by launching blockchain-enabled provenance tracking for its wool and cashmere supply chains. It also expanded its sustainable fiber portfolio through partnerships with regenerative agriculture initiatives. These actions reinforce its reputation for quality and environmental stewardship while strengthening its influence in the premium segment of the global textile market.

- Inditex, through its integrated supply chain and agile manufacturing mode, has redefined fast fashion textiles in Europe and worldwide. Headquartered in Spa, the company controls fabric development, ddesigningand garment production across Southern Europe and North Africa. Rec, Inditex accelerated its sustainability roadmap by scaling the use of recycled polyester and organic cotton across all brands. It also invested in waterless dyeing technologies and launched a garment collection and recycling program in all EU stores. These initiatives enhance its operational resilience and align with tightening EU regulations on circularity and chemical management.

- Lenzing Group is an Austrian leader in eco-friendly cellulosic fibers, including Tencel and Lenzing Ecovero. The company supplies sustainable alternatives to cotton and polyester to brands across Europe, North America a nd Asia. It also partnered with major retailers to develop closed-loop recycling systems for post-consumer textiles. Through continuous innovation in bio-based materials and low-impact production, Lenzing plays a pivotal role in advancing the global textile industry’s decarbonization and circularity goals.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the Europe textile market are prioritizing vertical integration to secure raw material access and reduce lead times. They are investing heavily in digital technologies such as AI-driven design and IoT-enabled production for greater efficiency. Sustainability is central to strategy, with companies adopting certified fiber, waterless dyeing, and chemical recycling. Many are reshoring or nearshoring manufacturing to mitigate supply chain risks and comply with EU due diligence laws. Collaborations with start-ups, research institutions, and waste management firms are accelerating circular business models. Brand transparency through digital product passports and blockchain traceability is becoming standard to meet consumer and regulatory demands. These multifaceted strategies collectively enhance competitiveness, resiliency, and alignment with Europe’s green industrial policy framework.

MARKET SEGMENTATION

This research report on the europe textile market is segmented and sub-segmented into the following categories:

By Application Type

- Clothing

- Industrial/Technical Applications

By Material Type

By Process Type

- Woven Textiles

- Non-Woven Textiles

By Country

- Germany

- Italy

- France

- United Kingdom

- Spain

- Rest of Europe

link